LANDING

▶ ▶ ▶

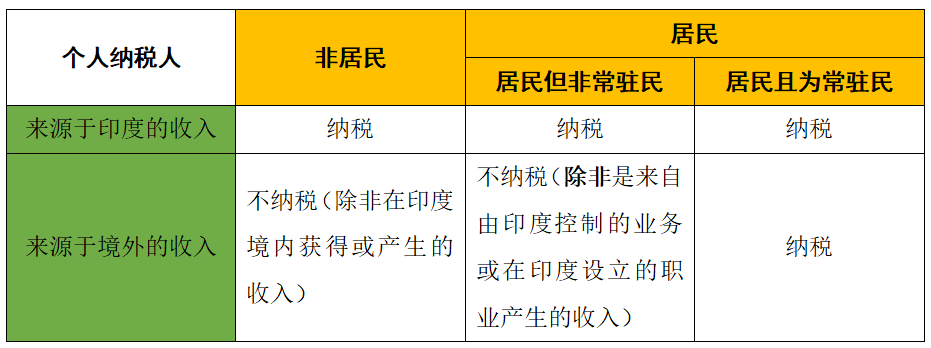

在印度,个人所得税的纳税义务人被细分为居民纳税人和非居民纳税人。不同类型的纳税义务人,所承担的纳税义务是不相同的。

一、如何判断居民身份?

二、外派到印度工作的中国公民的个人纳税义务

1、印度个人所得税的缴纳

外派到印度工作的中国公民在印度是否有义务缴纳印度个人所得税,是取决于该公民在4月1日至次年3月31日的财政年度在印度的停留时间,无论国籍或居留目的是什么。

从上文我们可以得知,印度的个人纳税人分为“居民”和“非居民”;居民又可分为“居民但非常驻民”和“居民且为常驻民”。

因此,外派到印度工作的中国公民在印度境内获得的收入,都需要缴纳印度个人所得税,而印度境外的收入则根据以上对应的类型进行缴纳。

【案例】

根据印度1961年《所得税法》和中印税收协定,张某在印度境内逗留天数为180天(不满182天),属于印度的非居民纳税人。李某在印度境内逗留的天数为280天,是印度的居民纳税人,且属于“居民但非常驻民”。因此,两人的纳税义务不同。

2、中国个人所得税的缴纳

那也有一个疑问,就是外派到印度的中国公民的收入是否需要缴纳中国的个人所得税?如果需要,应该怎样进行纳税申报?

附中印的部分个人所得税法条:

《个人所得税法》

第一条 在中国境内有住所,或者无住所而一个纳税年度内在中国境内居住累计满一百八十三天的个人,为居民个人。居民个人从中国境内和境外取得的所得,依照本法规定缴纳个人所得税。

第七条 居民个人从中国境外取得的所得,可以从其应纳税额中抵免已在境外缴纳的个人所得税税额,但抵免额不得超过该纳税人境外所得依照本法规定计算的应纳税额。

《境外所得个人所得税征收管理暂行办法(2018修正)》

第七条 纳税人受雇于中国境内的公司、企业和其他经济组织以及政府部门并派往境外工作,其所得由境内派出单位支付或负担的,境内派出单位为个人所得税扣缴义务人,税款由境内派出单位负责代扣代缴。其所得由境外任职、受雇的中方机构支付、负担的,可委托其境内派出(投资)机构代征税款。

第九条 中国境内的公司、企业和其他经济组织以及政府部门,凡有外派人员的,应在每一公历年度(以下简称年度)终了后30日内向主管税务机关报送外派人员情况。内容主要包括:外派人员的姓名、身份证或护照号码、职务、派往国家和地区、境外工作单位名称和地址、合同期限、境内外收入状况、境内住所及缴纳税收情况等。

印度:

《Income-tax Act,1961》

Section-5 Scope of total income.

5. (1) Subject to the provisions of this Act, the total income of any previous year of a person who is a resident includes all income from whatever source derived which—

(a) is received or is deemed to be received in India in such year by or on behalf of such person ; or

(b) accrues or arises or is deemed to accrue or arise to him in India during such year ; or

(c) accrues or arises to him outside India during such year :

Provided that, in the case of a person not ordinarily resident in India within the meaning of sub-section (6)* of section 6, the income which accrues or arises to him outside India shall not be so included unless it is derived from a business controlled in or a profession set up in India.

(2) Subject to the provisions of this Act, the total income of any previous year of a person who is a non-resident includes all income from whatever source derived which—

(a) is received or is deemed to be received in India in such year by or on behalf of such person ; or

(b) accrues or arises or is deemed to accrue or arise to him in India during such year.

Explanation 1.—Income accruing or arising outside India shall not be deemed to be received in India within the meaning of this section by reason only of the fact that it is taken into account in a balance sheet prepared in India.

Explanation 2.—For the removal of doubts, it is hereby declared that income which has been included in the total income of a person on the basis that it has accrued or arisen or is deemed to have accrued or arisen to him shall not again be so included on the basis that it is received or deemed to be received by him in India.

Section-6 Residence in India.

6. For the purposes of this Act,—

(1) An individual is said to be resident in India in any previous year, if he—

(a) is in India in that year for a period or periods amounting in all to one hundred and eighty-two days or more ; or

(b) [***]

(c) having within the four years preceding that year been in India for a period or periods amounting in all to three hundred and sixty-five days or more, is in India for a period or periods amounting in all to sixty days or more in that year.

Explanation 1.—In the case of an individual,—

(a) being a citizen of India, who leaves India in any previous year as a member of the crew of an Indian ship as defined in clause (18) of section 3 of the Merchant Shipping Act, 1958 (44 of 1958), or for the purposes of employment outside India, the provisions of sub-clause (c) shall apply in relation to that year as if for the words "sixty days", occurring therein, the words "one hundred and eighty-two days" had been substituted ;

(b) being a citizen of India, or a person of Indian origin within the meaning of Explanation to clause (e) of section 115C, who, being outside India, comes on a visit to India in any previous year, the provisions of sub-clause (c) shall apply in relation to that year as if for the words "sixty days", occurring therein, the words "one hundred and eighty-two days" had been substituted 30[and in case of 31[such person] having total income, other than the income from foreign sources, exceeding fifteen lakh rupees during the previous year, for the words "sixty days" occurring therein, the words "one hundred and twenty days" had been substituted.]

Explanation 2.—For the purposes of this clause, in the case of an individual, being a citizen of India and a member of the crew of a foreign bound ship leaving India, the period or periods of stay in India shall, in respect of such voyage, be determined in the manner and subject to such conditions as may be prescribed.32

33[(1A) Notwithstanding anything contained in clause (1), an individual, being a citizen of India, having total income, other than the income from foreign sources, exceeding fifteen lakh rupees during the previous year shall be deemed to be resident in India in that previous year, if he is not liable to tax in any other country or territory by reason of his domicile or residence or any other criteria of similar nature.]

34[Explanation.—For the removal of doubts, it is hereby declared that this clause shall not apply in case of an individual who is said to be resident in India in the previous year under clause (1).]

(2) A Hindu undivided family, firm or other association of persons is said to be resident in India in any previous year in every case except where during that year the control and management of its affairs is situated wholly outside India.

(3) A company is said to be a resident in India in any previous year, if—

(i) it is an Indian company; or

(ii) its place of effective management, in that year, is in India.

Explanation.—For the purposes of this clause "place of effective management" means a place where key management and commercial decisions that are necessary for the conduct of business of an entity as a whole are, in substance made.

(4) Every other person is said to be resident in India in any previous year in every case, except where during that year the control and management of his affairs is situated wholly outside India.

(5) If a person is resident in India in a previous year relevant to an assessment year in respect of any source of income, he shall be deemed to be resident in India in the previous year relevant to the assessment year in respect of each of his other sources of income.

(6) A person is said to be "not ordinarily resident" in India in any previous year if such person is—

(a) an individual who has been a non-resident in India in nine out of the ten previous years preceding that year, or has during the seven previous years preceding that year been in India for a period of, or periods amounting in all to, seven hundred and twenty-nine days or less; or

(b) a Hindu undivided family whose manager has been a non-resident in India in nine out of the ten previous years preceding that year, or has during the seven previous years preceding that year been in India for a period of, or periods amounting in all to, seven hundred and twenty-nine days or less 35[; or

(c) a citizen of India, or a person of Indian origin, having total income, other than the income from foreign sources, exceeding fifteen lakh rupees during the previous year, as referred to in clause (b) of Explanation1 to clause (1), who has been in India for a period or periods amounting in all to one hundred and twenty days or more but less than one hundred and eighty-two days; or

(d) a citizen of India who is deemed to be resident in India under clause (1A).

Explanation.—For the purposes of this section, the expression "income from foreign sources" means income which accrues or arises outside India (except income derived from a business controlled in or a profession set up in India)] 36[and which is not deemed to accrue or arise in India].

【声明】

以上内容具有较强的时效性,且不构成法律意见或建议。

点击上方 ''印度兰迪LANDING''关注公众号

文/凌茹琳 审/谢晓晶

▶ ▶ ▶